The Strait of Hormuz is far more than a narrow maritime corridor—it is one of the most consequential arteries of the global energy ecosystem. For supply chain leaders, it represents a convergence point of geography, geopolitics, and economic continuity. Under stable conditions, the movement of crude oil, gases, and refined products through this route appears seamless. Yet, as Sanjay Desai, Independent Board Advisor and Mentor, observes, rising geopolitical tensions can swiftly destabilize freight flows, insurance frameworks, and refinery planning cycles. In today’s volatile environment, Hormuz is no longer just a passage—it is a defining variable in global supply chain strategy.

The Strait of Hormuz occupies a uniquely critical position in the global energy ecosystem. For supply chain professionals, it is not simply a geographic connection between the Persian Gulf and the Arabian Sea—it is the central artery through which energy security for multiple continents is maintained. Every day, millions of barrels of crude oil and large volumes of natural gas and refined products pass through this narrow channel, linking upstream production hubs in the Gulf with downstream consumption centres across Asia and beyond.

In periods of relative geopolitical calm, this movement appears almost routine. Tankers move in predictable cycles, refining systems operate with precision, and supply chains function with a high degree of coordination. This creates an illusion of permanence—that the system is stable and self-sustaining. However, this stability is conditional. It depends on uninterrupted passage, predictable risk environments, and confidence among shipping and insurance stakeholders.

The moment this confidence is shaken, the system begins to respond. Freight markets react almost instantly, reflecting increased risk premiums. Insurance costs escalate as underwriters reassess exposure. More importantly, operational decisions begin to shift—shipowners reconsider routes, charterers delay commitments, and refineries start preparing for potential feedstock variability.

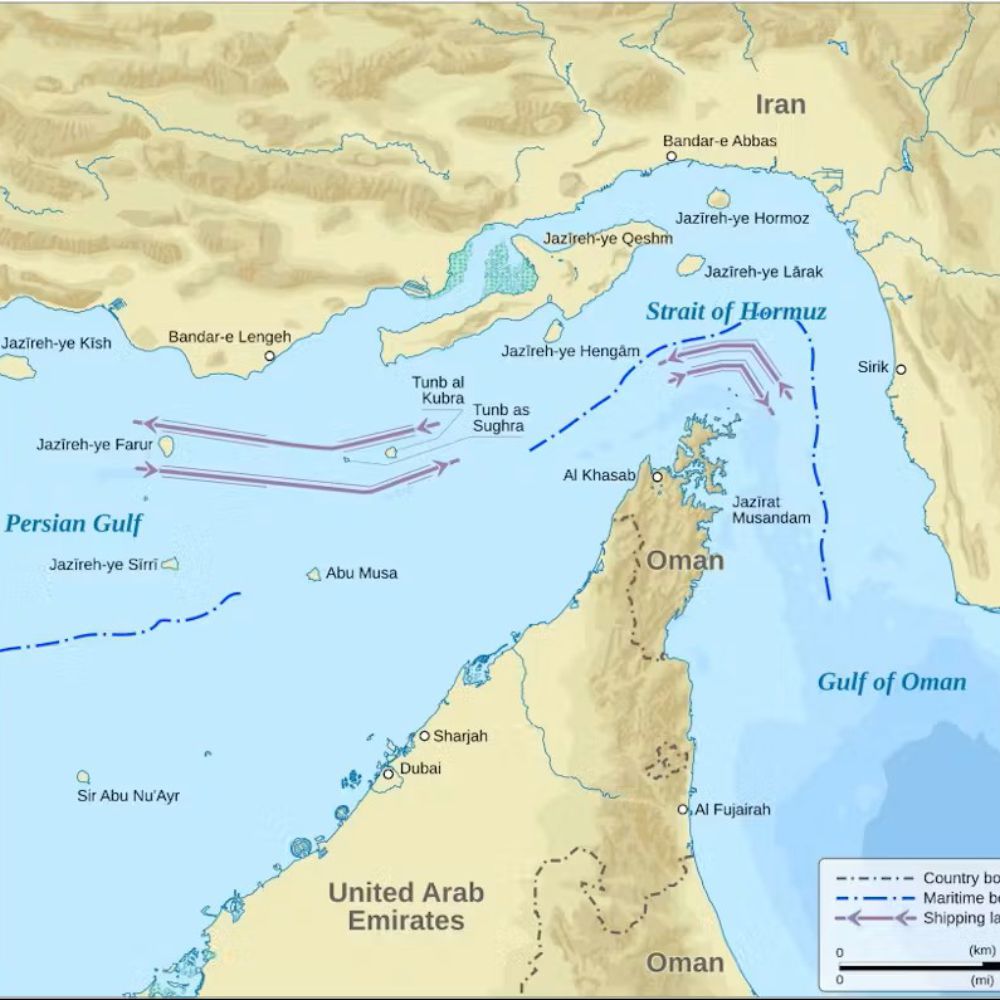

Geographically, the vulnerability is evident. The strait stretches roughly 167 kms, with widths ranging from 55 to 95 kms, narrowing to around 30–32 miles at its most constrained point. Within this confined passage lies one of the highest concentrations of energy trade globally. This combination of narrow geography and high throughput creates a structural imbalance—efficiency on one hand, fragility on the other.

The dependency is also bilateral. Gulf producers depend on Hormuz to access global markets, while importing nations—particularly in Asia—depend on it for sustained energy supply. This creates a tightly coupled system where disruption is not isolated—it is shared. A blockage or slowdown affects both ends simultaneously, amplifying its impact across the global energy value chain. Even though international legal frameworks classify Hormuz as a transit passage that should remain open, supply chains are governed by behavior, not just law. If stakeholders perceive risk, usage declines—effectively constraining the corridor without formal closure. This is what makes Hormuz uniquely critical: it is as much a psychological chokepoint as it is a physical one.

WHY THE STRAIT MATTERS

The Strait of Hormuz matters because it represents a convergence of scale, concentration, and irreplaceability. It is not merely a transit route—it is the primary gateway through which the Gulf region connects to global energy markets. Nearly 20% of global oil trade flows through this corridor, alongside significant volumes of liquefied natural gas. Such concentration is difficult to replicate elsewhere. While multiple maritime routes exist globally, very few carry such a high share of a critical commodity through such a constrained passage.

This creates a structural vulnerability within the global energy system. From a supply chain perspective, it functions like a single high-capacity artery supporting multiple economic systems—where even short-term disruption can trigger cascading effects across markets, industries, and geographies. Its importance is further reinforced by the limited scalability of alternatives. Pipelines and secondary routes can absorb a portion of the flow, but they fall short of matching the flexibility, capacity, and cost efficiency of maritime transit through Hormuz.

Governance adds another layer of complexity. International law defines shared coastal sovereignty, with Iran to the north and Oman to the south, and shipping lanes passing through overlapping territorial waters under the transit passage regime of the United Nations Convention on the Law of the Sea (UNCLOS). While this framework protects navigational rights, actual vessel movement is influenced far more by real-time safety assessments, insurer risk thresholds, and prevailing geopolitical signals.

WHO DEPENDS ON HORMUZ

Asia holds the greatest dependency on the Strait of Hormuz, making it one of the most regionally concentrated yet globally consequential supply chain risks. Data indicates that nearly 85–90% of crude oil and gas exports transiting through this corridor are destined for Asian markets. This dependency is particularly pronounced in major economies such as China, India, South Korea, and Japan. Each of these economies is structurally tied to consistent energy inflows, and in many cases, a significant proportion of their imports rely directly on this single maritime corridor.

China, as the world’s largest crude importer, depends on uninterrupted flows to sustain its vast manufacturing base and industrial output. Even minor disruptions can ripple through production cycles, logistics systems, and export commitments. India, with its rapidly growing economy and increasing energy consumption, relies on steady inflows not only for industrial production but also for transportation, agriculture, and consumer energy needs. South Korea and Japan face an even more acute challenge. With limited domestic energy resources, their reliance on imports is near total. This makes them highly sensitive to any disruption in shipping routes, as alternatives are limited and often more expensive. Their refining systems are optimized for steady inflows, leaving little room for sudden variability.

The dependency is not limited to importers alone. Gulf producers are equally reliant on Hormuz to move their products to global markets. This creates a dual-sided dependency—exporters depend on it to sell, and importers depend on it to consume. Even economies with relatively lower direct exposure, such as the United States, are affected through global pricing mechanisms and freight market dynamics. Oil is a globally traded commodity, and disruptions in one region quickly translate into price volatility worldwide.

This interconnected dependency transforms Hormuz into more than just a regional chokepoint—it becomes a global pressure point, where disruptions affect both supply and demand simultaneously, amplifying their impact across the entire energy value chain.

HOW DISRUPTION SPREADS

The impact of disruption in Hormuz unfolds in a layered and often accelerated manner, beginning with perception and extending into physical supply chains. The first layer is psychological. Markets react almost instantaneously to geopolitical developments. Traders, analysts, and financial institutions begin pricing in risk, leading to immediate increases in crude oil prices. Freight rates rise as shipping companies factor in uncertainty, and insurance premiums escalate as underwriters reassess exposure. These reactions often occur before any physical disruption takes place, highlighting the anticipatory nature of global markets.

The second layer is operational. Shipping behavior begins to change. Tankers may delay entry into the strait, wait offshore for clearer signals, or reroute through longer and more expensive pathways. Charterers and shipowners reassess risk exposure, while insurers impose additional conditions or higher premiums. Even when the strait remains technically open, the flow of goods slows due to caution and uncertainty.

The third layer is industrial. Refineries, which operate on tightly synchronized schedules, begin to experience disruptions in feedstock supply. Delayed shipments can lead to reduced throughput, inefficiencies in production, and adjustments in output. This affects the availability of refined products such as diesel, jet fuel, LPG, and petrochemicals. The fourth layer is systemic. The impact spreads across industries. Aviation faces fuel supply uncertainties, logistics costs increase, manufacturing output slows, and consumer prices begin to rise. What starts as a maritime disruption evolves into a broader economic challenge.

Importantly, this cascading effect is not linear—it is amplified by the interconnected nature of modern supply chains. A delay in one segment quickly propagates across multiple sectors, creating compounding effects. This is what makes Hormuz uniquely critical. Disruptions here are not contained— they spread rapidly, affecting global markets, industrial systems, and end consumers alike.

WHY HORMUZ BECOMES UNSTABLE

The instability of Hormuz is rooted in a complex interplay of geography, geopolitics, and perception. Geographically, the strait is narrow and heavily trafficked, making it inherently sensitive to disruptions. The high density of vessel movement within a confined space increases the risk of congestion, delays, and operational incidents.

Geopolitically, the region surrounding Hormuz has long been characterized by tension and strategic rivalry. This creates an environment where even minor incidents—whether naval activity, political signaling, or isolated security events—can escalate quickly and impact shipping operations. However, one of the most critical drivers of instability is perception. Supply chains operate on confidence. If shipowners, operators, or crews perceive heightened risk, their behavior changes. Vessels may avoid the route, delay transit, or operate under stricter safety protocols. Interestingly, recent insights indicate that insurance availability is not the primary limiting factor. Organizations such as the Lloyd’s Market Association continue to provide war-risk coverage. However, operational decisions are driven more by safety concerns and risk assessments than by insurance capacity alone.

This leads to what can be described as “soft disruptions”—situations where the strait remains open in principle but constrained in practice. Traffic declines, transit times increase, and costs rise, even without a formal blockade. This dynamic reflects a broader shift in global supply chains, where uncertainty and perception can be as disruptive as physical barriers. Managing such risks requires a more nuanced understanding of both operational and behavioral factors.

ALTERNATIVES AND RESILIENCE

Alternatives exist, but none can fully replace the Strait of Hormuz. Gulf exporters have developed bypass routes such as Saudi Arabia’s East-West pipeline to the Red Sea, the UAE’s export corridor to Fujairah, and Iran’s Jask terminal. These pathways provide critical fallback options and reduce exclusive dependence on Hormuz during periods of disruption. However, their role remains complementary rather than substitutive. The limitation is structural. These routes cannot absorb the full volume that typically transits through Hormuz, nor can they match the flexibility and speed of maritime flows under stable conditions. Capacity constraints, higher operating costs, and longer transit times mean that while rerouting is possible, it is neither immediate nor economically equivalent.

This is where the challenge for supply chain planning becomes evident. Diversion strategies offer relief, but only to a certain extent. They introduce additional lead times, logistical complexity, and cost variability. In a disrupted scenario, the system does not stop—but it slows, fragments, and becomes more expensive to operate. On the demand side, resilience is built through a different set of levers. Major consuming economies are increasingly focusing on diversified sourcing portfolios, strategic petroleum reserves, and greater flexibility in refining configurations. The ability to process a wider range of crude grades allows refineries to adapt more quickly when supply patterns shift.

Contract structures and inventory strategies are also evolving. More flexible agreements, multi-supplier arrangements, and optimized stockholding policies provide a buffer against short-term disruptions. Supplier diversity, in particular, reduces overdependence on any single region or route. A visible example of this shift can be seen in European markets, where countries are actively reducing reliance on single-region sourcing. By integrating supplies from the Gulf, the United States, Africa, and the North Sea, they are building a more balanced and resilient energy mix.

AMIDST CURRENT DEVELOPMENTS, ONE SHINING EXAMPLE IS INDIA

Amid the evolving dynamics of global energy supply chains, India stands out as a compelling example of strategic adaptation and resilience. Over the past few years, India has actively worked to reduce its dependence on any single crude supply route, including Hormuz. This has been achieved through a deliberate strategy of diversifying its supplier base. Today, India sources crude oil from nearly 40 countries, significantly reducing its exposure to route-specific disruptions.

A key component of this strategy has been the increased import of Russian crude. These shipments often take alternative routes, such as via the Suez Canal or around the African continent, bypassing Hormuz entirely. This not only enhances supply security but also introduces greater flexibility into the system. In parallel, India has invested in refining flexibility, enabling its refineries to process a wider range of crude grades. This adaptability allows for rapid adjustments in sourcing strategies in response to geopolitical developments.

The result is a more resilient and responsive supply chain—one that is less vulnerable to disruptions in any single corridor. India’s approach reflects a broader shift in supply chain thinking—from cost optimization to resilience optimization. It demonstrates that proactive planning, diversification, and flexibility can significantly mitigate the risks associated with critical chokepoints like Hormuz.

TAKEAWAYS FOR SUPPLY CHAIN PROFESSIONALS

For supply chain professionals and policymakers across global companies and government institutions, the appropriate response is not reactive decision-making, but measured, forward-looking action. The situation around the Strait of Hormuz reinforces the importance of staying anchored in planning discipline rather than short-term reactions. Energy supply chains require structural depth. This includes developing multiple sourcing avenues, enabling alternate logistics routes, and maintaining inventory buffers that can absorb short-term disruption. Dependence on a single corridor, regardless of historical reliability, creates exposure that becomes visible only when the system is under stress.

Planning approaches also need to evolve. Linear models built on predictability are increasingly insufficient in a volatile environment. Supply chains must be capable of adjusting sourcing decisions, rerouting cargo, and recalibrating operations with speed and precision. Responsiveness is no longer a secondary capability—it is central to continuity. Cost evaluation requires a more nuanced lens. Routes that appear economically efficient in stable conditions can carry significant downside when exposed to disruption. Delays, price volatility, and operational inefficiencies can quickly offset initial savings. Decision-making, therefore, needs to account for both cost and exposure.

Across governments, enterprises, and institutions, there is a visible shift toward diversification, operational flexibility, and stronger coordination across the value chain. The objective is not to eliminate uncertainty, but to ensure that supply chains continue to function effectively when conditions change. At its core, the lesson from Hormuz is about maintaining composure while strengthening preparedness—ensuring that continuity is driven by structured planning rather than reactive response.

DESIGNING FOR CONTINUITY, NOT JUST EFFICIENCY

The real lesson from the Strait of Hormuz is not simply that critical routes carry risk—it is that modern supply chains have been built with a level of concentration that amplifies that risk. The issue is less about a single chokepoint and more about how dependent global systems remain on a limited set of pathways. Addressing this requires a shift in how supply chains are designed and governed. Instead of relying on stability as a baseline, organisations need to operate with variability as a constant. This means rethinking sourcing strategies, building optionality into logistics networks, and enabling faster decision-making through better visibility and coordination.

Energy supply chains, in particular, sit at the core of broader economic activity. Any disruption in crude or gas flows quickly extends into refining, transportation, manufacturing, and end consumption. Strengthening these linkages—rather than treating each segment in isolation—becomes critical to maintaining continuity. Looking ahead, the competitive edge will not come from the lowest-cost route or the most optimised network. It will come from systems that can adapt without breaking—absorbing shocks, reconfiguring flows, and sustaining operations under pressure. Hormuz, in that sense, is not just a risk point. It is a signal of what the future demands: supply chains that are not only efficient in calm conditions, but fundamentally designed to perform in uncertainty.

Categories

Categories