“Supply chain management has shifted its goals from volume maximization and cost minimization to optimum operations and sustainability of operations and profits. Supply chain is more and more looking at improving efficiencies, customer needs, goals of multiple stakeholders, green technologies, sustainability thru alternate fuels or recycling and making the cement industry future ready,” envisages JVB Sastry, independent consultant, in an interview.

How has the cement industry performed in the recent past given the Covid pandemic scenario and how do you see the dynamics shaping up from here on?

The installed capacity of the Indian cement industry is close to 545 million tons and is the second largest in the world after China. The utilization share of cement production capacity in India at the end of fiscal year 2019 was just over 70%. This was the highest utilization share during the observed timeframe. The production volume in that year was over 330 million metric tons. After seeing modest growth in demand between 4-6% y-o-y, the industry has witnessed a steep growth of more than 13% in the year 2019. There has been a renewed push in many sectors including Infrastructure and Housing. All this has come to a standstill in the year 2020 due to Covid. The lockdown across the country has halted the supply chain and sales even though some of the units continued with minimum production levels, considering that it is a process industry. From the month of May, there is resumption of economic activity and the industry has recovered due to pent up demand and good rural demand. Demand recovered quickly to 79% of last year's volumes in May and 93% in June led by a strong rural demand aided by three consecutive good monsoons, adequate availability of local labor and lower spread of Covid-19 than in urban areas. The industry took a big hit on volumes and profitability in Quarter I and II of this fiscal but with demand revival, higher utilization and stable prices, the operating profits for most of the firms is expected around 20%. However, there are headwinds in the environment in terms of rising costs of raw materials and fuel/pet coke, which may erode the profitability to some extent.

However, the Covid impact is expected to be on more systemic and structural issues such as how the industry adapts to the post-Covid digitization and changes in business trends. That will be a challenge to both the business and supply chain leaders of the industry to adapt to the new normal and bring in a few desired changes in the vintage systems and processes that the industry follows in supply chain and sales. Hopefully, there will be positive changes in adapting newer technology to connect with suppliers and customers and bring in synergies in supply chains so as to optimize physical movement and save costs and improve efficiencies. Much depends upon the revival and sustaining demand and creative and matured responses of the industry to the changing demand and customer expectations.

What are the unique characteristics of SCM in the cement industry?

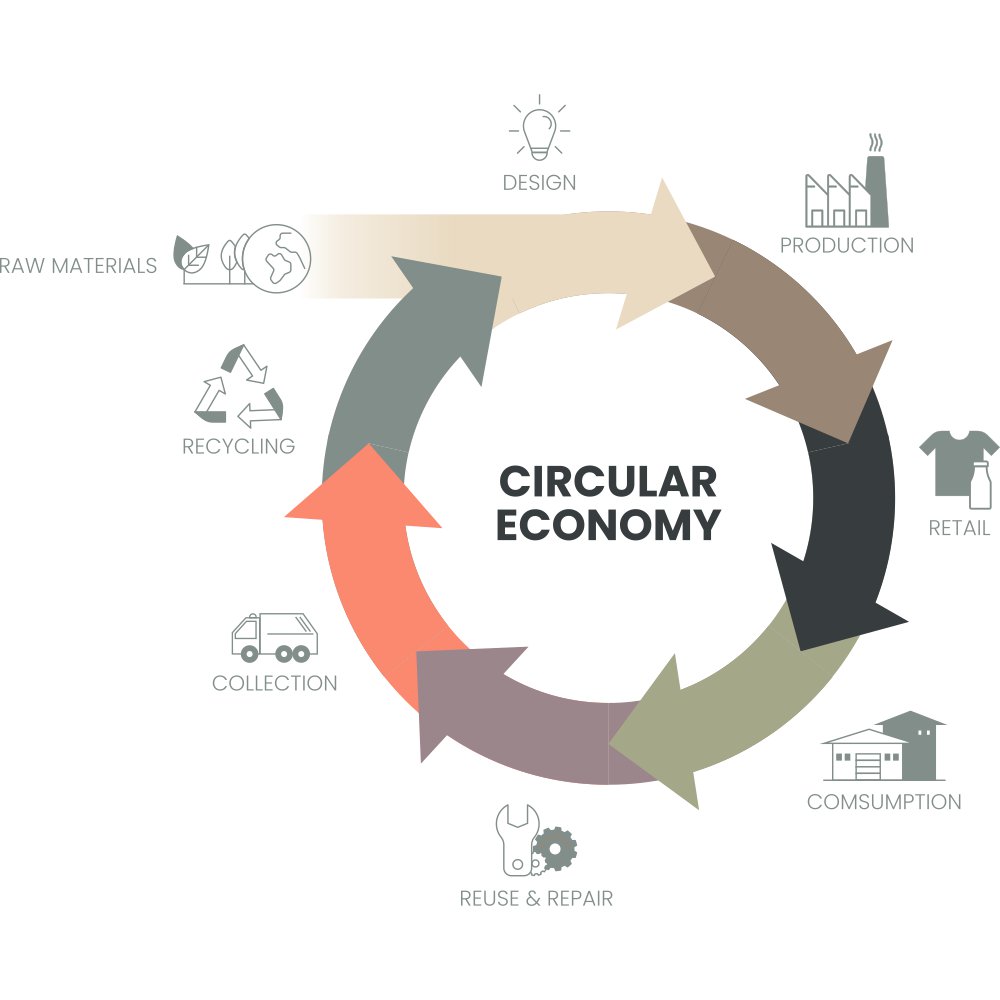

Simply put, supply chain management is the handling of the entire production flow of a good or service — starting from the raw components all the way to delivering the final product to the consumer. Given this framework, SCM in cement Industry is evolving from a distribution, volume game to that of market /demand linked to meet customer expectations. Some of the unique characteristics of SCM are: Supply chain management in the cement industry is moving away from supply centric to demand centric. Planning for operations and strategic planning of manufacturing and distribution footprints is happening more and more based on understanding the markets & customer needs and using the decision-making tools such as optimizers and simulation tools.

Supply chain management has shifted its goals from volume maximization and cost minimization to optimum operations and sustainability of operations and profits. Supply chain is more and more looking at improving efficiencies, customer needs, goals of multiple stakeholders, green technologies, sustainability through alternate fuels or recycling and making the cement industry future ready. In the recent decades, the Industry has made remarkable progress in the manufacturing front by adopting energy efficiency, reduction in CO2, using AFR, achieving zero/negative water utilization rates and many other technological improvements/innovations.

On the business side, the industry has focused mostly on volume peaking and distribution. However, now the change in this sphere too is happening thru customer focus, efficiencies, cost optimization, adopting technology in logistics, using environment-friendly products like blended cements, direct to market sales reducing the physical travel and multiple handling of a cement bag, encouraging more and more bulk cement in place of bag cement, thereby cutting back use of Polypropylene and saving environment.

All these changes have come about due to the industry adopting the sound principles of a good supply chain management and aligning its business operations through a cross functional collaboration and planning.

Some of the other characteristics are as follows:

The Cement industry is a freight and raw material intensive industry. Supply chain management needed to be accorded a strategic role & position. However, only lately, this function is getting its due place and that too mainly with an objective to reduce costs or tide over temporary shortages in input materials.

Further, seamless integration of business processes is important and is recognized by many cement companies, still functional dominance especially that of primary functions like manufacturing and sales is prevalent, often resulting in sub-optimal outcomes.

The industry faces twin challenges of demand and supply volatility both in availability and prices.

The production and distribution planning are centralized given the commodity nature of the business.

The industry has recently adopted optimization tools for operations planning and resource allocation, which is a good sign. However, the industry suffers from volume centric approach giving undue emphasis upon cost reduction as opposed to cost optimization.

Cement is sold to both B2B and B2C markets. However, the central supply chain approach of the industry is to achieve efficiency, cost reduction often ignoring the customer service level optimization/cost-service tradeoffs which are essential in a customer facing /retail market. This poses a unique challenge to its supply chain management to balance conflicting goals such as cost and service.

Another characteristic of the supply chain is the high local sourcing quotient in the overall procurement spend. This limits the scope for global sourcing strategies except in high value /global commodities like coal/pet coke.

The cement industry uses high quantities of flyash/slag as blending materials in the production of PPC and PSC. However. the industry has failed to upgrade its storage/ transport infrastructure for these important raw materials resulting in high logistics costs in sourcing these. Many-a-times, this JIT approach to important raw materials also disrupts production due to sudden shortages /non availability.

How complex is the cement supply chain and how do you manage these complexities?

Logistics safety is an all Important and critical complex issue facing all supply chains. This aspect is not given much importance in India compared to cost and other supply chain issues. However, the human cost of injuries and fatalities cannot be measured in terms of lives, impact on morale and business disruptions. Many progressive cement companies in India are focusing on this aspect and working on this thru Driver safety/training programs, vehicle fitness checks, in-plant layouts and design, which are oriented for better safety, GPS monitored vehicle movement, rewarding and punishing driver safety records and many other measures. This is most welcome and must be fully encouraged. Demand volatility is a complexity. Seasonality, festivals, and other local disruptions cause sudden dips and peaks in demand.

The industry tries to overcome this thru better production planning, field/intermediate warehousing, split manufacturing facilities by keeping grinding units close to the markets so that clinker is produced and stored in the GU for cement manufacturing as per demand levels.

Another complexity is its high cost of logistics, both on inbound and outbound side. Many steps are taken to optimize sourcing and logistics thru multi modal transport, use of large fleet and freight rationalization, return loads and other tactical steps. The industry has also embarked upon SWAP operations with competitors thru legal processes so that leads are reduced for moving inputs and at times finished goods too. This has reduced the cost complexity for the Industry to some extent.

Talking about the supply side, volatile costs of pet coke, flyash, slag put a huge cost and availability risk to the industry. Increased use of AFR, long term contracts, hedging, use of pod ash or pond slag are some of the mitigating steps taken by the industry. Fuel cost and its impact on freight is another complexity and the industry will do well to study switching to CNG or alternate fuels where available. Lighter aluminum boded trucks are also being tried out by a few leading cement companies to reduce fuel consumption and thereby the freights. In the long run, using Sea/ river logistics will help the industry reduce logistics costs to a greater extent, besides it helping to reduce motor pollution. The industry is working on many fronts to mitigate supply chain complexity by keeping the chain lean, reduce the intermediaries thru direct sales to markets from the plants and focus on customer, profitability and sustainability.

What steps should companies take to circumvent the Covid pandemic and keep the wheels of growth moving through efficient supply chain?

The Industry will do well to adopt online marketing/selling and digitize loading/ storage and dispatch information. The Industry needs to help its dealers to adopt these technologies and help reduce the transactions costs. Similarly, as is being done in a few Asian countries, fast setting concrete might help reduce the time taken for construction and this would help tide over shortage of construction labor at sites. Demand stimulation is being attempted by the government thru various schemes. The industry may tie up with banks and other institutions and improve target delivery of cement and products to customers with help of credit /loan facilities extended by these institutions. In the same way, the cement companies can work closely with infrastructure projects to make cement/ concrete as per requirements and help in faster delivery and improve ease of transactions.

What are the approaches to innovative supply chain strategies in cement industry?

The Industry has taken several innovative steps to improve efficiencies, reduce cost and improve service. Some of the major ideas have been:

Splitting clinkering and grinding units so as to reduce the cost of raw material logistics in making clinker and at the same time grinding cement closer to markets to reduce the last mile cost and achieve on time-in-full deliveries to customers.

Demand based end-to-end optimization of production and distribution has helped the industry to optimize volumes & cost and reduce lock in working capital.

The other innovation is One Horse and two trailer transport model which helps improve truck turnaround and also helps the trailer to act as a mobile warehouse for small lot sales in semi urban and rural markets has been a success.

Constant innovations in packaging both in type of packing materials and its denier has been a silent improvement, which has contributed to cost reductions.

Use of Red mud, Bauxite rejects, coal tailings and many other such cheaper options have helped the industry reduce costs and sourcing risks.

The Industry is also working on facility sharing and integration of inbound and outbound supply chains to improve availability and reduce costs.

Leveraging mobile technology for printing invoices at mobile warehouses to sending delivery SMS alerts has been a low-cost innovation that the industry has adopted many years ago.

The supply chains in some of the cement companies have tried semi-mechanization in unloading and loading of cement bags at warehouses and railheads. This has helped improve productivity and reduce the physical stress on labor. This needs to be improved and adopted on a wider scale.

The Cement industry has still a long way to go in innovating the way cement is packed, stored, handled sold and delivered. The industry has to leverage technology, AI and other tools. The market side supply chain is still vintage with lack of transparency and high transaction cost.

What are the technological advancements you have implemented in supply chain?

This is work in progress. To recount some of the important ones in the recent past:

Auto packers which helped faster and accurate loading

Online Bag printing that helps MRP printing before loading, thereby eliminating large pre-loading MRP based bag inventory

RFID at Plants and reduced the Driver/Plant touch points, paperbased operations and improved Gate In gate Out

GPS for all trucks on main routes, which helped improve truck safety, reduce accidents, improve TAT and helped share transit information with customers

Mobile app-based logistics training to logistics team members is another area, which helped learning at convenience and reduced cost.

The industry will do well to try many such technology tools that aid in handling, storage/retrieval of cement and increase online sales.

What is the right supply chain for cement?

On the demand side, the two main streams of sales for the cement industry are Bag cement sales and BULK/RMC sales. The first one is to retail customers and the second one is largely to Institutional and Infrastructure project customers. Supply chain strategies, tools and processes need to be adopted suitable for these major segments. Efficiency and cost reduction are primary with service in case of B2B segment. In case of bag cement sales to retail customers, service, ease of delivery with cost optimization are important. On the supply side, the right supply chain is to work on cost, sustainability, and risk mitigation.

How can SCM generate Value in the cement industry?

SCM in cement industry has immense contribution. some of the important deliverables are:

End-to-end cost optimization

Securing volatile supplies to the plants

Planning for a volatile demand market and mitigate stock outs and /or stock gluts

Help optimize inventory & reduce lock up of working capital thru better planning and improved efficiencies.

The industry incurs more than 70% of its costs on logistics and sourcing. Supply chain management's contribution to optimize/reduce this cost even by 3-5% will boost the bottom line of the industry. This is critical as the industry often suffers from price erosion for its finished products due to volatile demand and competition. Supply chain in the cement industry generates both tangible value in terms of improvement in EBITDA thru cost reduction and in many intangible areas such as customer satisfaction, loyalty, brand equity and long-term business growth.

How can we work towards developing sustainable supply chain for the cement sector?

The country at large can make its contribution for a sustainable supply chain by

Using more and more bulk cement and reduce packaging waste

Using more blended cements, thereby reducing clinker percentage, Co2 and help increase use of flyash and slag, which are byproducts of power and Steel industries.

Other Industries should help share costs in delivery of waste materials for use in the Industry as Alternate fuel required delivery platforms in handling these AFR materials, which are often hazardous and expensive.

What does the future hold for supply chain?

The future augurs very well for the cement industry's supply chain, both for its strategic/critical role it plays and for its contribution. There are many headwinds in the business environment like:

Global trade is increasingly becoming uncertain with many embargos, unrests, and epidemics. This will impact sourcing of pet coke/imported coal. Similarly, import/export of clinker /gypsum can also come under stress for similar reasons. Supply chain needs to work towards alternatives/fall back options to overcome these uncertainties.

Logistics safety is also coming under scrutiny as the country becomes more stringent with road safety rules including ban on overloading of trucks. Supply chain has to find ways to ensure high safety standards and also optimize fleet size and freights.

The supply chain has to adopt many new technologies and bring in change. It has to foster a culture of seamless integrations thru transparent communications and collaboration. It has to train and develop cement business managers to know all aspects of the business and work for long-term sustainability and growth. Supply chain needs to engage with all internal and external stakeholders to understand and bring in changes the way backend and front-end of the business works.

Limestone quarries, coal mines, raw material sourcing will remain a challenge in operations and cost & supply chain needs to bring in required changes for better efficiencies here.

Online sales are ushering in a revolution in Indian business and cement industry supply chain needs to adapt new processes and tools to manage this transition.

Supplier partnering and co-development has to be ushered in so that there is enough for all stakeholders. otherwise the Sea-Saw game of' I win-You-lose 'way of transacting business will continue with its many problems and toxic business culture.

Categories

Categories